ROF Book Club: Money Master The Game — 7 Simple Steps To Financial Freedom

ROF Book Club: Money Master The Game — 7 Simple Steps To Financial Freedom

I read this book not once, but three times — each time more slowly than my previous attempt — before deciding that I had a decent enough grasp of it to write about it, and for good reason: It is a MONSTER.

All 638 pages of it .

Yes, yes I know’s this book’s been out there for quite awhile, but given my current funemployed state, I thought why not read every book I had that I haven’t already read (of which I have way too many — let’s just say I’ve been known to buy books on a whim and put off reading them for long periods of time) or just simply want to read again?

So here we are and oh yes, welcome to the first ever ROF Book Club entry: The 10 Lessons I learned from Tony Robbins’ Money Master the Game: 7 Simple Steps To Financial Freedom.

LESSON #1: The life you want may cost less than you think.

What’s the price of your dreams? Is it a million ringgit? 10 million ringgit? A billion?

He says that for many of us, the life that we want seems so out of reach because we tend to put an impossible number on it.

It’s not that we shouldn’t dream big, but because we make this number so much bigger than it needs to be, we end up disbelieving our ability to reach it and reject it subconsciously (hello, self-sabotaging behaviours!).

To arrive at a realistic number, Robbins uses Maslow’s hierarchy of needs as a starting point. This takes into consideration your:

Basic needs like food, water, shelter, rest and security. In other words, certainty.

Psychological needs like intimate relationships and feelings of accomplishment, or significance.

Self-fulfillment needs like achieving one’s full potential and being able to spend time on creative pursuits.

He then uses this hierarchy to dissect most people’s financial dreams (assuming that not everybody wants the same thing) into five incrementally higher levels that will need different sets of numbers to reach:

1. Financial security: At this level, you’re generating enough investment income to cover the bare bones of your living expenses (ie shelter, food, transportation, utilities and the like) for the rest of your life.

2. Financial vitality: Here, you have enough investment income to cover your basic living expenses plus a little extra for indulging in the little luxuries in life, like eating out at Michelin-star restaurants or monthly trips to the spa.

3. Financial independence: Congrats! The tables have turned and money is now officially your slave so you no longer have to work to maintain your current lifestyle.

4. Financial freedom: Unlocking this level of financial nirvana means being financially independent and being able to afford a couple more significant luxuries like traveling several times a year or buying that sports car you’ve been eyeing.

5. Absolute financial freedom. You’ve reached the highest level of financial heaven. This is being able to do anything you want, whenever you want, anywhere you want, give freely (fancy buying someone you love the home of their dreams or setting up a charity of your own?) and live completely on your own terms — all without having to work another day in your life.

Which financial dream does yours look like and how much you need to make it happen?

In Money Master The Game, Robbins encourages using ‘real world’ numbers (ie your actual expenses instead of a random 7-figure number).

The upside of doing this is more of a mental one than anything: It’ll help you create the mental space to develop the confidence and self-belief to actually achieve your dream and perhaps, shoot for the stars and beyond once your basic needs are being met on autopilot.

LESSON #2: Money is not the end goal.

On the surface, it may look like just numbers that you’re chasing, but beneath it all, it’s so much more than that.

Money is far from the end goal, says Robbins. “What we’re really after are the path to money: The places money can take us, the time, freedom and opportunity money can bring — these are what we’re really after.”

It’s about living life on your own terms.

And as for all the money you accumulate? “It’s not really yours and you can’t take it with you when you die.”

As far as he’s concerned, you’re just the caretaker for these riches and someone else will eventually take it.

The key takeaway here? Yes, the goal is financial freedom, but this freedom shouldn’t come at the expense of your well-being, relationships and peace of mind.

Earn it, grow it and learn how to master it, but don’t let money control you.

LESSON #3: Watch out for those fees.

Before we jump into the shark-infested waters of this touchy subject, let me start off by saying this: Yes, any company that provides a valuable service to its customers should be compensated for what they do.

As far as investment services go, this compensation usually comes in the form of a percentage-based fee, which seems fair. After all, the more money they make you, the more they should be compensated to reflect their efforts, right? Right. At least I think so, but feel free to disagree.

Except that in the finance industry, not all investment services are created equal and neither are their returns. And more often than not, these services get to bite a sizable chunk out of your capital every single year regardless of whether they make you any money or not.

In fact, even when they’re bleeding cash, the service provider still gets paid…at a loss to you. And if you decide to withdraw your cash, there’s — you guessed it — another fee you’ll probably have to pay for that too.

It doesn’t take a genius to figure out who’s at the losing end in this equation.

And let’s not get started on how the majority of active fund managers fail to beat their benchmarks. (read: They’re not making you as much money as they should be).

Therein lies the contemptuous issue of ‘investment fees’ that often comes with actively managed unit trust funds, or mutual funds in U.S speak.

The bottom line is this: Fees (usually in the form of sales charges and annual management fees, which can go up to 5.5% and 1.9% respectively) eat away at your returns (or capital, if your fund isn’t generating any returns). The higher the fees, the less money you make over the long term.

And for the average investor who’s got limited capital to start with, these fees can make a huge difference in their future financial standing.

If you’re inclined to think that these fees don’t add up to much, here’s how big a chunk just 1% in annual fees can wipe out from your returns :

")

In Money Master The Game, Robbins recommends bypassing these fees altogether by investing in low-cost exchange traded funds that do away with sales charges and bloated management fees altogether — a direction in which I’m moving towards myself.

And now with affordable, exchange traded funds (ETF)-based roboadvisors like StashAway, Akru and MyTheo as well as international online brokers like Interactive Brokers, Tiger Brokers, Tradestation Global and FSMOne at our fingertips, those of us in Malaysia who want to diversify away from high-fee investment services, can.

Having invested in unit trust funds for well over a decade, I’m more aware than ever of how their fees have been a huge drag on not just my capital growth, but annual investment income, and this is something I’m working on changing.

LESSON #4: Make your money train go faster.

The premise behind Money Master The Game is to build your own personal ATM that provides you an income for life.

Getting this ATM up and running requires that you first save up a critical mass of cash that in big enough numbers, will work for you to generate enough income that you can live on instead of you having to work for it.

Let’s say you’ve figured out what your financial dream looks like and what it’ll take to get there. The next logical step you’ll need to sort out is this: How long will it take you to get there?

Enter the rule of 72, which tells you how long it’ll take for your investment to double based on a fixed annual rate of return (or interest rate). To get the estimated ‘doubling timeline’, just divide 72 by your investment’s annual rate of return.

What you’ll get is a timeline that looks something like this:

This means that if you’re just chucking all your money in a fixed deposit account, you’re looking at about 36 years to double your capital and a very, very long road to retirement (although I 100% would have done this if I were earning throughout the 1980s and early 90s, when deposit interest rates in Malaysia were as high as 10-14%).

Oh, how times have changed.

Robbins’ advice when it comes to using the rule of 72? Get better at picking investments that give you higher returns while costing you as little as possible (not to sound like a broken record, but you guessed it: Like ETFs).

This, along with earning more money, increasing your savings and investment rates, and optimizing your lifestyle so that you’re not overspending on things that aren’t making your life better will get that personal ATM train moving faster and more efficiently.

Obviously, the younger you are when you start doing this, the better off you’ll be since you’ll have more time on your side to get that train chugging and eventually, running at full speed.

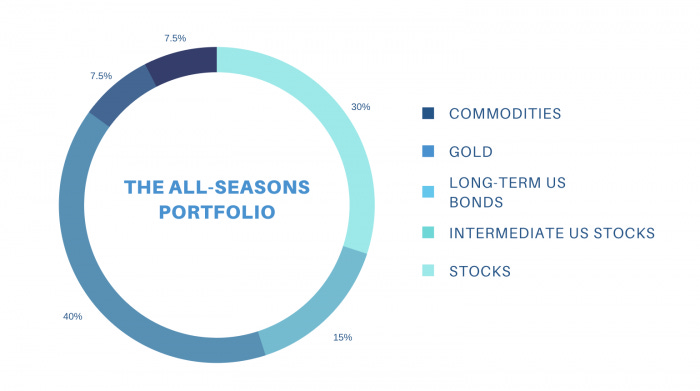

LESSON #5: Asset allocation is everything.

Robbins defines asset allocation as this: “It means dividing up your money among different classes or types of investments (such as stocks, bonds, commodities and real estate) and in specific proportions that you decide in advance according to your goals or needs, risk tolerance and stage of life.”

The ultimate goal of asset allocation? To increase your upside returns while decreasing your risk. In other words, not putting all your eggs in one basket.

In Money Master The Game, he introduces us to the All-Seasons Portfolio, a vastly simplified version of the stress-tested All-Weather Strategy modeled by Ray Dalio, who founded Bridgewater Associates — 2021’s third largest hedge fund in the world, and one that’s reaped an average return of 11.1% for its investors over the decades.

This particular portfolio was designed to take into account the following economic environments:

Higher than expected inflation (rising prices).

Lower than expected inflation (or deflation).

Higher than expected economic growth.

Lower than expected economic growth.

When translated into a portfolio the average person like you and me can implement, it looks a little like this:

30% stocks, which are three times more risky than bonds.

15% intermediate (7-10 year) term and 40% long-term (20-25-year) US bonds to counter the volatility of stocks.

7.5% each in gold and commodities which also have high volatility but can counter the poor performance of stocks and bonds during times of rapid inflation.

The most practical way to implement this portfolio, says Robbins is with (again), low-cost ETFs.

5 thoughts that came to mind while reading this book:

Are the 5 financial dreams listed above realistic for most Malaysians given their suppressed wages?

How much bigger would my nest egg be if I had invested in ETFs over the last 20 years instead of unit trusts? The thought of getting an answer to this one genuinely scares me.

For those of us who’re working our asses off day and night juggling multiple jobs, money has to be the end goal, at least for the time being, right? This is how it was for me at many points during my career.

Will the All-Seasons Portfolio work for most people, anywhere in the world? Any licensed financial planners or advisors who can share their 2 cents?

How can this portfolio be adapted to the Malaysian investment landscape…or should it not be to begin with, given how small the Malaysian market is in comparison to the U.S and the rest of the developed world?

There seems to be something missing from the All-Seasons Portfolio: Alternatives like cryptocurrencies and peer-to-peer lending (to be fair, this book was published in 2014). Should these have a place in it or are they considered too risky for most folks who are living paycheck to paycheck and can barely save up enough cash to invest? Ray Dalio has since shared his thoughts on Bitcoin and its competitors here.

What do you think?

As for my own financial future, there’s only one thing that comes to mind when I think about growing my wealth for a the foreseeable future: ETFs.

Recommended Tools & Resources

*Note: These suggestions contain affiliate links, which means that I’ll earn a small fee if you decide to use them. Using these links won’t cost you anything extra, but it’ll allow this blog to earn some money. If you use them, thank you 🙂

STASHAWAY

StashAway puts my cash to work by diversifying it into baskets of global exchange-traded funds (ETFs) safely and easily according to my risk appetite minus the freakishly high sales and management fees that come with unit trust funds. Sign up here to save 50% on management fees when you invest up to RM100,000 for your first 6 months.

THE MILLIONAIRE NEXT DOOR by Thomas J. Stanley and William D. Danko

This is the very first book I ever read about money, and one that opened my eyes to what it really means to be wealthy and how the true rich (ie people who have a lot of money and are smart with it) make, manage and use the green stuff.

YOUR MONEY OR YOUR LIFE by Vicki Robin

I consider this mandatory reading for everyone, no matter where you are on your financial journey. If you’ve got questions about how to develop good habits around tricky subjects like debt, earning, spending and your relationship with money, this book’s got the answers.

THE 4-HOUR WORK WEEK by Timothy Ferriss

This isn’t a personal finance book per se, but it is about making money in ways that have nothing to do with working a 9-5 job and introduced me to the idea of mini retirements. If lifesyle design is your thing, this is a must read.

Feature photo by Pawel Kadysz on Unsplash